Commercial insurance has its own language, and most of it isn't written down anywhere a founder can find it. You'll hear "BOR" in your first carrier call and nod like you know what it means. You'll get a question about whether your platform supports "IVANS download" and feel the floor tilt. You'll watch a deal stall because someone said "non-admitted" and you didn't catch the implication.

This glossary is the cheat sheet I wish someone had handed me. Fifty-plus terms, grouped by where they actually show up in your day. Each one gets a plain-English definition, why founders should care, and where you'll trip over it in practice.

Bookmark this. Link to specific terms. Share it with new hires.

Key Stakeholders

Carrier

What it is: The insurance company that underwrites the risk and pays the claims. Travelers, Chubb, The Hartford, Liberty Mutual, AIG, GAIG, Hiscox. The capital is theirs; the policy is on their paper.

Why founders care: Carriers are the source of supply. Every product you sell, every quote, every bind, runs through one of them. Your distribution model is only as viable as the carriers willing to put paper behind it.

How it shows up: "Which carriers are you on?" is the second question any sophisticated partner will ask you. The first is what lines you write. No carriers, no product.

Retail Broker / Agent

What it is: The broker that sits across from the insured business and places their coverage. Marsh and Aon at the top, HUB and Acrisure and USI in the middle, and tens of thousands of independent agencies in small commercial. "Agent" usually implies a captive relationship with one carrier; "broker" implies independent placement across multiple carriers. The terms get used interchangeably in casual conversation.

Why founders care: Retail brokers and agents own the customer relationship. If your model touches the insured, you'll either disintermediate retail (hard) or partner with retail (more common). Either way, understanding their economics is non-negotiable.

How it shows up: "We have 200 retail agency relationships" is the kind of number that wins partnerships. The retail channel still controls the majority of US commercial premium.

Wholesaler / Wholesale Broker

What it is: The intermediary between retail brokers and carriers, especially for risks that don't fit standard admitted markets. RT Specialty, Amwins, CRC, Burns & Wilcox. A retail broker brings a hard-to-place account to a wholesaler, who shops it across surplus-lines and specialty carriers.

Why founders care: Wholesale is where the harder, larger, more lucrative risks live. If your product is aimed at retail-only small commercial, wholesale is irrelevant. If you're touching anything specialty, wholesale is the buyer.

How it shows up: "We placed it through Amwins" means the retail broker couldn't find admitted capacity and went to E&S via a wholesaler.

MGA (Managing General Agent)

What it is: A delegated-authority firm acting on behalf of one or more carriers. MGAs typically have authority to bind coverage, set pricing within carrier-defined parameters, and sometimes handle claims, all on the carrier's paper without being the carrier themselves. Compensated via commission and often a profit-share/override.

Why founders care: "Become an MGA" is the most common platform-building move in insurtech. It lets you control underwriting, pricing, and product without raising the capital to become a carrier. But MGA economics are tighter than they look, and carrier appointments are harder to win than they sound.

How it shows up: Almost every modern insurtech is structurally an MGA, even if they market themselves as a "platform" or "marketplace."

MGU (Managing General Underwriter)

What it is: Narrower than an MGA in theory. An MGU typically has delegated underwriting authority — quote, set pricing within parameters, bind — but not the broader administrative authority an MGA may carry (claims handling, full distribution authority, sometimes premium collection). The label distinction has eroded in practice: many firms operate as MGUs but call themselves MGAs because MGA is the more recognized term, and many MGAs technically lack claims authority. The functional question is what authorities the contract actually grants, regardless of which acronym appears on the masthead.

Why founders care: If a carrier offers you an "MGU" arrangement instead of an "MGA" arrangement, read the contract. The authorities you actually get — bind, claims handling, premium collection, product modification, sub-appointment — matter more than the label on the agreement. Some carriers use "MGU" specifically when they want to retain claims handling, which has real economic implications: claims handling is one of the most operationally expensive parts of running an insurance program, and not staffing it changes your cost structure meaningfully.

How it shows up: A founder describes their company as an MGA in pitches, but the underlying contract is technically an MGU agreement without claims authority. The distinction doesn't matter for the pitch deck. It matters when they want to differentiate the program through claims experience and discover they can't.

Reinsurer

What it is: The insurance company that insures other insurance companies. Munich Re, Swiss Re, Hannover Re, Everest. Carriers cede a portion of their risk to reinsurers in exchange for ceded premium. Reinsurance comes in two main flavors: treaty reinsurance (a standing agreement covering a defined class of business, most common), and facultative reinsurance (placed risk-by-risk for individual large or unusual accounts). MGAs typically build their capacity stack with reinsurer capital fronted by a primary carrier. The primary "fronts" the paper (so the policy is admitted and rated) while the reinsurer takes most of the economics and most of the risk.

Why founders care: If you're building a program or MGA, your capacity structure usually depends on reinsurer support. Reinsurer appetite — for your class, your geography, your loss results, and the macroeconomic moment — determines whether the program exists at all. Reinsurer pricing and terms reset on an annual cycle (most treaty renewals happen January 1, with smaller cycles April 1, June 1, and July 1), which means MGAs often discover next year's program economics only a few weeks before they need to commit to writing it.

How it shows up: An MGA founder mid-year says "we have committed capacity for the next two years." That's strong. An MGA founder in November says "we're waiting on 1/1 renewals." That's the honest answer, and it means next year's capacity, pricing, and terms aren't locked yet.

Insured

What it is: The business (or individual) whose risk is being underwritten and who the policy will pay if a covered loss occurs. Distinct from "policyholder" (the named contract holder on the policy, usually but not always the same as the insured) and from "additional insured" (a separate party named on the policy to receive coverage for liability arising from the named insured's operations). In a master policy structure, common in PEOs and association programs, the policyholder and the insured are different entities.

Why founders care: Founders use "insured," "policyholder," "client," and "customer" interchangeably. They're not the same. The insured is the entity whose loss the policy pays. The policyholder holds the contract. The customer of an insurtech is often the broker or platform partner, not the insured. Getting these terms right matters in legal, compliance, and product contexts. Additional-insured endorsements in particular have driven a meaningful chunk of commercial litigation in the past decade.

How it shows up: In a PEO arrangement, the PEO is the policyholder on a master WC policy; the client businesses are the insureds. A landlord requires a tenant to add the landlord as additional insured on the tenant's GL policy. The tenant is the insured, the landlord is the additional insured, and a covered claim by a visitor against the landlord can now be tendered to the tenant's carrier.

Market Structure

Admitted

What it is: A carrier licensed in a given state, with rates and forms filed and approved by the state insurance regulator. Admitted carriers participate in the state guaranty fund: if they go insolvent, the state covers claims up to a limit. Most standard commercial business runs on admitted paper.

Why founders care: Whether your product is admitted or non-admitted determines which brokers can sell it, who can buy it, and how fast you can iterate on form and rate. Admitted means slower changes (state filings) and broader distribution. Non-admitted means faster iteration and narrower distribution.

How it shows up: "Is this admitted?" is the first question a retail agent asks when you bring them a new product.

E&S

What it is: Excess & Surplus lines. Carriers not licensed in the state, accessed through surplus lines brokers, used when the admitted market won't write the risk. Also called surplus lines or non-admitted. Rate and form flexibility is far higher (no state filings), but coverage isn't backed by the guaranty fund, and only surplus-lines-licensed brokers can place it. Most surplus-lines transactions also pass through a state stamping office, a quasi-regulatory body that reviews and stamps policies for compliance with surplus-lines eligibility rules.

Why founders care: E&S is where new products get tested, where harder risks get placed, and where most insurtech innovation happens, because the regulatory loop is shorter. If you're building a novel coverage, you're almost certainly starting in E&S.

How it shows up: "We're surplus lines only" means broader product flexibility, narrower broker network, and a surplus-lines tax (typically in the low to mid single digits, varies meaningfully by state) layered onto every policy.

Hard/Soft Market

What it is: The two phases of the underwriting cycle. A hard market is one of constrained capacity, rising rates, narrowing terms, increased underwriting scrutiny, and carriers exiting classes or geographies. What insureds experience as "premiums going up and coverage getting worse." A soft market is the opposite: abundant capacity, falling rates, broadening terms, eager underwriting. Markets harden line by line and geography by geography, not uniformly.

Why founders care: The market cycle is the single largest external variable in commercial distribution economics. A platform that launched in a soft market may have built its growth math on rates that no longer exist; a platform launching in a hard market sees capacity providers more selective about new MGA partnerships. Whether your insureds renew with you, switch, or shop is significantly cyclical. Most insurtech founders underestimate how much of their early growth was tailwind from a hardening market.

How it shows up: A retail agency's renewal book in the recent property hard market showed double-digit rate increases across most lines without producer effort. That's the cycle doing the work. The same book in a softening market shows flat or declining renewal premium and producers having to fight for accounts that used to renew on autopilot.

Key Products

WC (Workers' Compensation)

What it is: State-mandated coverage for workplace injuries. Pays medical costs and lost wages for employees injured on the job. Required in nearly every state for nearly every employer with employees. Priced by payroll × class code rate, with experience modification (E-mod) for larger employers.

Why founders care: WC is the most heavily regulated, most data-rich, most workflow-intensive commercial line. It's also the most embedded. Payroll platforms like Gusto, Rippling, and ADP increasingly bundle WC. PEOs are essentially WC arbitrage businesses with HR layered on top.

How it shows up: Workers' comp comes up in literally every conversation about embedded insurance, payroll partnerships, or small-employer benefits.

BOP (Business Owner's Policy)

What it is: A package policy combining commercial property (the building, contents) and general liability into a single policy, designed for small-to-mid commercial businesses. The default product for restaurants, retail shops, small offices, small contractors. BOP is the package version; standalone Property and GL handle the same risks for businesses too large or too specialized for BOP.

Why founders care: BOP is the single largest small-commercial product. If you're building for small commercial, you're building for BOP first.

How it shows up: A 6-employee retail boutique buys one BOP and is largely covered. They don't think of it as "property plus GL." They think of it as "the business policy."

GL (CGL)

What it is: Commercial General Liability. Third-party liability coverage: bodily injury and property damage that the business causes to others. The "slip and fall" coverage. Standalone GL is less common than GL bundled into BOP; CGL standalone is typical for contractors, manufacturers, and businesses too large for BOP.

Why founders care: GL is the second-most-common commercial coverage after WC. Every business needs it; pricing varies enormously by class code.

How it shows up: A general contractor needs GL with specific additional insured endorsements before they can step on a job site.

Cyber

What it is: Coverage for data breach response, ransomware, business interruption from cyber events, regulatory fines, and (sometimes) social engineering fraud. A relatively young line whose underwriting has tightened sharply since the ransomware wave.

Why founders care: Cyber is the fastest-growing commercial line. Underwriting has shifted toward structured controls (MFA, EDR, security questionnaires). The data inputs are highly structured, which makes the line especially API-friendly. Lots of insurtech activity here.

How it shows up: A 100-person SaaS company gets quoted cyber and the carrier wants to scan their externally-facing infrastructure before binding.

Inland Marine

What it is: A confusingly named line covering property in transit, property on the move, and specialty property that doesn't fit standard property forms. Includes contractor's tools and equipment, fine art, electronic data processing equipment, transportation/cargo, and bailee's liability. Has nothing to do with the ocean. The name dates to when this line split off from ocean marine insurance in the 1800s.

Why founders care: Inland Marine has unusual underwriting flexibility (manuscript forms, individual valuation, no standard rating bureau) and has been one of the most profitable P&C lines for carriers. It fits embedded models well: equipment dealers, contractor platforms, freight brokers, and similar platforms sit on natural inventories of insurable property.

How it shows up: A contractor's $200K of tools and equipment is covered under an Inland Marine policy rather than their BOP. A photographer's $40K of camera gear, same. A trucking company's cargo, same.

Builders Risk

What it is: Property coverage during construction. Covers the structure being built, materials on site, and (sometimes) materials in transit, against fire, theft, weather, and other perils. Time-bounded: the policy starts at groundbreaking and ends at substantial completion. Specialized form because insurable value grows during the policy period as construction proceeds.

Builders Risk is technically a form of inland marine insurance — most builders risk policies are written on inland marine forms rather than commercial property forms — but distributed and underwritten as a distinct product with its own carriers, MGAs, appetite, and submission workflows.

Why founders care: Builders Risk is the standard coverage on every commercial and residential construction project, plus most renovations above a certain size. Distribution is fragmented and heavily wholesale-oriented.

How it shows up: A general contractor breaking ground on a $5M strip mall buys a 12-month Builders Risk policy with the project owner as named insured. The premium scales with completed value at takeoff plus materials on site.

Commercial Property

What it is: Standalone coverage for the buildings, equipment, inventory, and contents owned by a business. Pays out when fire, theft, vandalism, weather, or other covered perils damage physical assets. Sold standalone (vs. packaged into BOP) for businesses too large for BOP, businesses with cat-exposed locations, or risks needing bespoke coverage like high-value buildings or complex multi-location schedules.

Why founders care: Property is one of the largest commercial P&C lines by premium and one of the most cyclical. Cat-exposed property — coastal, wildfire zones, convective storm regions — has been through a sustained hard market, with capacity withdrawal and rate increases routinely in the double digits, often well into the 20%+ range annually in the most exposed zones. If your insureds have buildings, expect to navigate this market dynamic.

How it shows up: A 50,000 sq ft warehouse in Florida is bound at a $250K premium with a 5% wind deductible. Two years ago the same property bound at $90K with a 2% wind deductible.

Commercial Auto

What it is: Coverage for vehicles used in business: delivery vans, contractor trucks, sales fleets. Includes liability, physical damage, and various endorsements (hired/non-owned auto, MCS-90 for trucking).

Why founders care: Commercial auto is one of the hardest lines in the market. Loss ratios have been elevated for years, capacity is constrained, rates have risen sharply. If your insureds have vehicles, this will be a pain point.

How it shows up: A landscaping company with three trucks needs commercial auto, and the rate has probably risen 15–20% at the last renewal.

Umbrella / Excess Liability

What it is: A liability policy that sits above an insured's underlying liability policies (GL, Auto, Employers Liability, sometimes E&O). When an underlying limit is exhausted, the umbrella drops down to provide additional coverage. "Umbrella" technically refers to coverage that's broader than the underlying (drops down to cover gaps); "Excess" strictly means higher limits on the same coverage. The terms get used interchangeably in practice.

Why founders care: Umbrella attaches on top of almost every commercial insured of meaningful size. Underlying limits define the "attachment point"; umbrella limits stack on top. Capacity has been tight for years due to nuclear verdicts: jury awards of $10M+ that exhaust primary limits and pierce umbrella layers.

How it shows up: A trucking company carries $1M of underlying auto liability and $5M umbrella on top, for $6M total liability capacity. After a serious accident with a $4M settlement, $1M comes from the auto policy and $3M comes from the umbrella.

Professional Liability (E&O / MPL)

What it is: Coverage for claims arising from professional services rendered negligently or with errors. Distinct from GL: GL covers bodily injury and property damage; E&O covers financial loss from professional advice or service. MPL (Miscellaneous Professional Liability) is the catch-all flavor of E&O for professionals whose work doesn't fit a named profession-specific product: consultants, marketing agencies, IT services firms. Profession-specific E&O products exist for lawyers, architects/engineers, accountants, doctors (medical malpractice), and real estate agents.

Why founders care: E&O is required by almost every B2B services company before a Fortune 500 client will sign their MSA. MPL specifically is a strong fit for embedded models targeting professional services. The classes are heterogeneous, which makes underwriting harder but creates room for differentiated products. Founders conflate E&O with GL constantly.

How it shows up: A boutique branding agency needs MPL before signing a new enterprise client. A consultancy gets sued for bad advice and the E&O policy responds. GL would not.

D&O (Directors & Officers Liability)

What it is: Coverage for directors and officers of a company (and the company itself) against claims arising from their decisions in those roles. Covers defense costs and settlements for shareholder suits, regulatory actions, breach of fiduciary duty claims, and management decision lawsuits. Three coverage parts: Side A (individuals when company can't indemnify), Side B (company reimbursement), Side C (entity coverage, mainly for public companies).

Why founders care: D&O is essential for any company taking institutional money. Every VC term sheet requires it. Pricing varies dramatically with stage and exposure: a pre-revenue startup might pay in the low five figures, a growth-stage SaaS company in the high five to low six figures, and a pre-IPO company well into six figures or more. An active line for insurtech embedded in startup-adjacent platforms.

How it shows up: A startup closing a Series A buys D&O within days of close. The investor's term sheet requires it, often with specific minimum limits and a named lead carrier.

EPLI (Employment Practices Liability)

What it is: Coverage for claims by employees against the company: wrongful termination, discrimination, harassment, retaliation, FMLA violations, and wage-and-hour claims (though wage-and-hour is often excluded or sub-limited). Excludes WC (which is the no-fault statutory regime for workplace injuries) and ERISA-governed benefits claims (which require fiduciary coverage). Often packaged with D&O and fiduciary as "management liability" for small to mid-sized companies; sold as a standalone product for larger employers.

Why founders care: EPLI claim frequency is materially higher than D&O frequency. Most companies will face an employment claim long before they face a securities claim. Even claims that are clearly meritless run well into the five- and six-figure range in defense costs before resolution, because employment cases rarely dismiss at the pleadings stage. Particularly relevant for embedded HR and payroll platforms looking to bundle insurance: the data is already in the platform (headcount, payroll, employee turnover), the underwriting is structured, and the buyer is an HR or finance leader who already has the platform open.

How it shows up: A 40-person company gets a wrongful termination claim from a former VP. The EPLI carrier assigns counsel; defense costs hit six figures before the case settles for a fraction of demand. The company's premium roughly doubles at renewal.

Key Terminology

LOB (Line of Business)

What it is: The product category: Workers' Comp, BOP, GL, Commercial Auto, Cyber, MPL. Each LOB is its own world: distinct carriers, distinct underwriting questions, distinct regulatory regime, distinct workflows, distinct economics. "WC" and "Cyber" share almost nothing operationally except that they're both called insurance.

Why founders care: LOB count is the single biggest driver of operational complexity in commercial distribution. Adding a second LOB doesn't double your work. It more than doubles it. Each LOB requires its own carrier appointments, its own underwriting questions, its own appetite intelligence, its own ACORD forms, its own claims workflow. Founders who say "we'll launch in WC and add BOP in Q3" routinely miss that timeline by 12+ months.

How it shows up: "How many LOBs?" is the single question that calibrates how seriously to take an insurtech's stated GWP. A $50M single-LOB program is a meaningfully different business than a $50M multi-LOB program.

BOR (Broker of Record)

What it is: The broker of record is the licensed broker entity formally designated on a policy as the party authorized to transact with the carrier on behalf of the insured. The BOR is who the carrier communicates with, takes instructions from, services the account through, and pays commission to. Every policy has exactly one BOR at any given moment. A "BOR letter," signed by the insured, is the document by which that designation is established or transferred. The letter is the instrument; the BOR is the role.

Why founders care: BOR is the unit of competition in retail brokerage. Books of business are bought, sold, and benchmarked based on BOR control. Carriers communicate with the BOR, not the insured. If your platform isn't the BOR, you have no direct carrier access on those accounts and no claim on the commission. Any insurtech that wants to own the customer relationship and the commission economics has to either be the BOR itself (which requires the licenses and the operational capacity to service the account) or partner with brokers who are. "Disintermediating the broker" almost always means becoming the BOR.

How it shows up: A retail agency's "book of business" is the set of policies on which they are the BOR. When an account changes brokers, what changes is the BOR designation. The policy stays in force, the carrier stays the same, but the broker the carrier talks to and pays now flips. A competing broker presents better terms, the insured signs a BOR letter, and at the next touchpoint the new broker is the one fielding the underwriter's call.

Submission

What it is: The complete application package sent from a retail broker (or wholesaler) to a carrier or MGA requesting a quote. A submission typically includes the ACORD application(s), supplementals, loss runs (for accounts with prior coverage), and any required carrier-specific documents. "The submission" is shorthand for the entire bundle that an underwriter needs to underwrite the account.

Why founders care: Submission quality is one of the strongest predictors of bind outcomes. Underwriters quote what they can read and decline what they can't. Incomplete submissions sit in a queue; clean submissions get quoted same-day. Almost every workflow automation product in commercial distribution is, at some level, a submission improvement product: better ACORD extraction, automated loss run requests, supplemental pre-fill, document validation.

How it shows up: A retail broker emails the submission to three wholesalers. The one with the cleanest packaging gets the first response. The other two get back to the broker after the deal has already moved.

Indication vs. Quote

What it is: Two different stages of carrier feedback. An indication is an early, non-binding estimate of where pricing might land, sometimes called a "ballpark" or "indication of interest." A quote is a firm, bindable offer with specific terms, conditions, and pricing. Indications often come back same-day from a brief submission; quotes require the full submission and complete underwriting. Many E&S and specialty risks live in indication territory for days or weeks before the broker decides which carriers to push to formal quote.

Why founders care: Conflating indications with quotes is one of the most common founder mistakes when looking at funnel data. "Quote-to-bind" calculated on indications looks artificially low because indications never bind. They only convert to quotes that then convert to binds. Bind rate calculated on indications instead of quotes is meaningless.

How it shows up: A broker shopping a complex restaurant property risk gets indications from five carriers between $35K and $80K, then decides which two to take to formal quote. Only the formal quotes show up in bind-rate calculations.

Subjectivities

What it is: Conditions a carrier attaches to a quote that must be satisfied before the policy will bind. A quote can carry subjectivities like "subject to satisfactory inspection," "subject to receipt of signed application," "subject to MFA implementation" (common in cyber), "subject to roof replacement" (common in coastal property). Until all subjectivities are cleared, the quote is not bindable.

Why founders care: Subjectivities are where deals stall in the final stretch. The broker has a quote, the insured wants to bind, and three subjectivities need to be cleared before coverage attaches. Each subjectivity is its own mini-workflow: get the document, complete the action, send proof to underwriting, wait for sign-off. Insurtech products that compress subjectivity clearance — automated inspection scheduling, security-control attestation, document collection — solve a real bottleneck.

How it shows up: A cyber quote comes back with a $25K premium and four subjectivities: confirm MFA on email, confirm endpoint detection, confirm offline backups, sign the application. The broker has 14 days to clear them or the quote expires.

Appetite

What it is: What a carrier is willing to underwrite, by class of business, geography, size, loss history, and a dozen other dimensions. Appetite is part formal (eligibility rules) and part informal (the underwriter's read of the account). It changes constantly as carriers respond to loss results and market conditions.

Why founders care: Routing submissions to carriers with matching appetite is the single biggest unsolved problem in commercial distribution. Most "AI for insurance" products are, at their core, appetite-matching tools.

How it shows up: "Carrier X is out of appetite for roofing contractors in Texas" means submissions in that class will be declined or non-responded. A good wholesaler knows this without having to ask.

Appointment

What it is: A formal contract authorizing a broker, agent, or MGA to sell a specific carrier's products. Each appointment defines what the appointee can do — quote, bind, issue, service — on which products and in which states.

There are two flavors. Direct appointments are between the carrier and the appointed entity, carrying the deepest authority and the best commission economics. Sub-appointments are where a carrier appoints an MGA or wholesaler, who in turn writes business through retail brokers without those retailers being directly appointed to the carrier. The retailer effectively sits under the wholesaler's paper, the wholesaler's authority, and the wholesaler's economics.

Why founders care: Carrier appointments are one of the hardest things for an insurtech to acquire. Established carriers often require meaningful expected premium production (often in the millions), a multi-year commitment, or a track record in the line before they'll appoint a new MGA. Thresholds vary widely by carrier and class. Without appointments, you have nothing to sell. Sub-appointments through a wholesaler are usually the path of least resistance for new entrants — you can be operational in weeks instead of months — but come with commission haircuts, less control over claims handling, and less long-term capacity stability than direct appointments give you.

How it shows up: A new MGA pitching capacity gets the question: "Direct appointments or sub-appointed?" The answer signals seriousness. Direct appointments take 6–18 months to win and require the carrier to underwrite the MGA itself: financials, leadership, track record, controls. Sub-appointments through a wholesaler can be in place in weeks.

Scratch Agency

What it is: A retail agency built from zero: no acquired book of business, no inherited carrier appointments, no existing producers, no client list. A founder hangs a shingle, gets the P&C licenses, and starts pitching carriers and writing accounts one at a time. Distinct from an agency that's been acquired, inherited, or spun out of an existing operation with carrier relationships already in place. Every digital-native insurtech that decides to be its own retail broker is, structurally, a scratch agency.

Why founders care: Starting scratch is the hardest distribution path in commercial insurance and the most natural one for tech-first founders. The chicken-and-egg problem is brutal: carriers want production history before they'll appoint you; you can't produce without appointments. Most scratch agencies solve this by sub-appointing through a wholesaler or aggregator for the first 18–36 months while building the production track record that earns direct appointments. Networks like ISU, SIAA, Smart Choice, and Renaissance exist specifically to give scratch agencies aggregated market access, pooling their volume across hundreds of agencies to get appointments no individual agency could secure alone.

How it shows up: A founder pitches their insurtech as a "tech-enabled retail agency." That's a scratch agency with a software wrapper. The underwriter's first question isn't about the technology; it's "what's your production?" If the answer is "we just launched," the conversation either ends or pivots to a sub-appointment arrangement.

Market Access

What it is: The set of carriers, products, and capacity an entity can actually quote and bind business through. Market access is a combination of three things: carrier appointments (the legal authority), API integrations (the technical capability to transact), and underwriter relationships (the goodwill that gets your submissions read and prioritized). Without market access you can't write anything. With limited market access you write what you can find appetite for, not what your insured actually needs.

Why founders care: Market access is one of the most underrated moats in commercial insurance distribution. The companies pulling ahead aren't the ones with the slickest UI. They're the ones who can place hard-to-place risks because they have access competitors don't. "How is your market access?" is the question every founder building an MGA gets asked by capacity providers, retail partners, and acquirers.

How it shows up: A retail broker shopping a complex risk lists their "markets": the carriers they can credibly approach. A wholesaler with broader market access wins business that competitors literally cannot quote because they don't have the appointments, integrations, or relationships to even get a submission read.

Program Business

What it is: Insurance written for a specific niche or class — pest control contractors, dental practices, food trucks, ride-share fleets — typically through an MGA with delegated authority and bespoke product terms. The program operates as a book-within-a-book inside a carrier, with its own underwriting guidelines, its own pricing, often its own claims process, and an economic structure that ties the MGA's compensation to the program's loss results.

Why founders care: Vertical insurtech almost always means building program business. The defensibility comes from the program: niche product, niche distribution, niche data. A successful program creates compounding advantages: the loss data improves underwriting, better underwriting attracts better risks, better risks improve loss ratio, lower loss ratio earns more capacity and bigger overrides. Failed programs do the reverse and exit the market within 2–3 years.

How it shows up: "We have a program with Nationwide for dental practices" means there's a delegated underwriting arrangement, a defined class, and likely a profit-share tied to loss ratio. "We're launching a program for [vertical]" is what an insurtech founder says when they've moved past the marketplace stage into actually owning underwriting outcomes.

Class Codes

What it is: The numeric codes that classify a business for insurance purposes outside of Workers' Comp. Two systems dominate. NAICS (North American Industry Classification System, 6 digits) is the modern federal standard maintained by the US Census Bureau and updated every 5 years. SIC (Standard Industrial Classification, 4 digits) is the older system NAICS replaced, but it still appears at carriers running on legacy systems and in older program data. Same business, two codes: a small bakery is NAICS 311811 (Retail Bakeries) or SIC 5461.

Why founders care: Class codes drive carrier appetite and pricing across every commercial line except WC. Underwriting eligibility rules are typically NAICS-keyed: "this carrier writes BOP for NAICS 722XXX (restaurants) and 561720 (janitorial services), declines NAICS 484XXX (trucking)." Translating between SIC and NAICS — and translating natural-language business descriptions into the right code — is foundational for any product doing appetite matching or carrier routing.

How it shows up: A roofing contractor's submission gets declined because the broker entered NAICS 238XXX (specialty contractors) instead of 238160 (roofing contractors) specifically. The carrier writes general specialty trades but not roofers.

NCCI Codes

What it is: A separate classification system, used only for Workers' Comp. The National Council on Compensation Insurance maintains a system of 4-digit class codes used in 38+ states. NCCI assigns a code to every type of work — 8810 for clerical office staff, 5645 for residential carpentry, 0042 for landscape gardening, 7219 for trucking — and publishes a base rate per $100 of payroll for each code in each state. That base rate, multiplied by payroll, multiplied by the insured's experience modification, is essentially the WC premium.

A handful of states don't use NCCI. The four monopolistic states — Ohio, Wyoming, North Dakota, and Washington — run state-administered WC funds with their own classification systems. California, New York, New Jersey, and a few others maintain independent rating bureaus that mirror NCCI but with state-specific modifications. Underwriting WC nationally means handling NCCI plus roughly seven independent state systems.

Experience modification (E-mod or X-mod) is the other major lever. It's a multiplier on the base rate, calculated from the business's loss history versus what would be expected for its class code. 1.0 means "exactly as expected." 0.85 is a 15% discount. 1.25 means paying 25% over base rate. Only businesses above a state-set premium threshold qualify for an experience mod.

Why founders care: WC classification is one of the most data-rich problems in commercial insurance: rates are publicly filed, class definitions are exhaustive, and the system is unusually well-defined compared to other lines. Mis-classification is also one of the most common pricing errors. A general contractor classified as a roofer (5645) can pay several times what they should. A logistics company classified as trucking (7219) instead of warehousing has a wildly different rate. This is one of the most active areas of insurtech tooling.

How it shows up: A small business gets a WC quote that seems inexplicably high. The cause is almost always class code: either misclassified, or correctly classified into an expensive class the business owner doesn't think describes their work. "What's your class code?" is the second question a WC underwriter asks, after "how many employees?"

Premium Audit

What it is: End-of-policy reconciliation of actual exposure against the exposure estimated at bind. Most prominent in WC (where premium is payroll × rate) and GL (where premium is often sales or payroll × rate). At policy inception the insured provides estimated payroll or sales; at policy end (or sometimes mid-term), the carrier audits actual exposure. Underestimated exposure results in additional premium owed; overestimated exposure results in a refund.

Why founders care: Audits are one of the most contentious touchpoints in the entire policy lifecycle. Insureds get audit invoices months after a policy expires and don't understand them. Agencies field dozens of audit disputes per year. Any product touching small-commercial WC or GL hits this wall. Pay-as-you-go WC (carriers like Hourly, AP Intego) was built specifically to eliminate the audit surprise: payroll integration means premium is collected in real time against actual payroll.

How it shows up: A landscaping company estimates $400K payroll at bind. Actual payroll comes in at $550K. The audit produces a $4,200 additional premium bill nine months after the policy started. The owner calls the agency yelling.

AM Best Rating

What it is: A financial strength rating issued by AM Best, the dominant rating agency for insurance carriers. Ratings run from A++ (Superior) down to D (Poor) with intermediate steps. A-rated and above is the practical floor for most commercial business. Anything below is treated as "non-rated" or "below admitted standard" by most sophisticated buyers. AM Best also publishes a "Financial Size Category" (FSC) ranging from I to XV based on policyholder surplus, often quoted together with the letter rating (e.g., "A VIII").

Why founders care: AM Best rating is a gating criterion for distribution. Many large brokers, sophisticated insureds, and contractually-required relationships (lender requirements, lease requirements, vendor compliance) require A- or better. A carrier with a strong product but a B+ rating cannot win business it would otherwise be priced to win. For MGAs picking capacity, the fronting carrier's AM Best rating directly affects which retail partners and which insureds the product can be distributed to.

How it shows up: A landlord requires every tenant to carry insurance from an A-rated carrier. The tenant brings a policy from an A- VIII carrier; it clears. The tenant tries again with a B++ carrier and the landlord rejects the COI.

Direct Bill vs. Agency Bill

What it is: Two ways carriers can collect premium. Direct bill means the carrier sends the bill straight to the insured and collects premium from them directly; the carrier then remits commission to the agency on a periodic statement. Agency bill means the agency bills the insured, collects premium from them, retains the commission, and remits net premium to the carrier. Most small commercial today is direct bill; mid-market and specialty is often agency bill.

Why founders care: The billing model determines who controls the cash, who manages collections, and which back-office workflows the agency has to run. Agency bill puts the agency in the middle of cash flow: they hold premium funds in trust before remitting, which means trust accounting requirements, collections risk, and reconciliation overhead. Direct bill is cleaner operationally but the agency loses visibility into payment status and has less leverage when carriers slow-pay commissions.

How it shows up: An agency switching a book of business from one carrier to another asks early: "Is this direct bill or agency bill?" The answer changes the operational footprint of writing that carrier's product.

Key Documents

ACORD Forms

What it is: Industry-standard forms maintained by ACORD (Association for Cooperative Operations Research and Development). The de facto data interchange standard between brokers and carriers. ACORD 125 is the commercial insurance application. ACORD 25 is the certificate of insurance. ACORD 130 is the WC application. There are hundreds.

Why founders care: Any product touching commercial insurance workflows touches ACORD. Brokers expect to submit ACORD forms; carriers expect to receive them. "ACORD-compatible" is table stakes; "ACORD-native" is a feature.

How it shows up: A retail agent emails a PDF of an ACORD 125 to your MGA inbox and expects you to extract the data. Fast.

Loss Runs

What it is: A carrier-issued report of an insured's claims history, typically going back 3–5 years. Lists each claim, date of loss, amount paid, amount reserved, and claim status (open / closed). Required for underwriting any account with prior coverage. Most underwriters won't quote without them. The insured (or their broker) requests loss runs from the current carrier; the carrier produces them, often after 5–15 business days.

Why founders care: Loss runs are the most common bottleneck in commercial submissions. The submission can't move until the loss runs arrive. Any product that compresses that loop — automated loss run requests, OCR/extraction from PDF loss runs, or carrier-direct claims data feeds — is solving an enormous workflow problem. Several insurtech companies have built their wedge entirely around this one document.

How it shows up: A retail broker can't get a renewal quote until the incumbent carrier produces loss runs. The submission stalls. The renewal slips. The broker calls the incumbent's service team for the fifth time to chase.

COI (Certificate of Insurance)

What it is: A one-page document evidencing that an insured has specific coverage in force. The ACORD 25 is the standard COI for liability coverage. It lists policy numbers, limits, effective dates, and (often) names a specific "certificate holder": the party requesting proof of coverage. A COI is evidence of coverage; it is not coverage itself.

Why founders care: COIs are the highest-volume document in commercial insurance. A general contractor needs one for every job site. A consultant needs one for every client engagement. A landlord requires them from every tenant. Most agencies generate hundreds per week, often as one-off requests with custom additional-insured language. COI issuance, tracking, and compliance verification is one of the most well-trodden wedges in agency tech.

How it shows up: A consultant signing an MSA gets an email at 4pm asking for a COI naming the client as additional insured with $2M limits by EOD. The agency has 30 minutes to issue it.

Endorsement

What it is: A mid-policy change to coverage. Adding a new vehicle to a commercial auto policy, raising a liability limit, adding an additional insured, changing a named insured: all endorsements. Each endorsement generates new policy documents and often a pro-rata premium adjustment. "Endorsement" can also refer to standardized coverage modifications that change the scope of the form itself, like a waiver of subrogation or a primary-and-non-contributory endorsement.

Why founders care: Endorsements are the most frequent transaction type in commercial insurance after COI issuance. A mid-sized retail agency processes endorsements daily across its book. Most carrier APIs handle quote and bind reasonably well and handle endorsements poorly. Many endorsement types still require email or portal-based requests. Endorsement automation is one of the largest unsolved problems in carrier connectivity.

How it shows up: A contractor adds a new truck to the fleet on Tuesday. The agency emails the carrier to request a vehicle-add endorsement. The endorsement issues Friday with a $400 pro-rata premium adjustment. Multiply by every change at every insured every week, and that's the workflow.

Declaration Page

What it is: The summary page of a policy: named insured, policy number, effective dates, coverage limits, premium, scheduled endorsements, and carrier. Usually the first page of the policy document. The "what was actually bought" snapshot. Almost always called "the dec page" in conversation, never the full name.

Why founders care: The declaration page is the canonical record of what coverage exists. AMS systems are largely organized around dec pages. Any product that ingests carrier policy data is parsing dec pages. Any product that validates contract compliance is checking dec page contents against requirements. Dec page OCR / extraction is a foundational capability for retail-facing insurtech.

How it shows up: A lender asks for "the dec page" to verify the borrower's property coverage before closing. Not the whole policy. Just that one summary page that proves what's in force.

Supplementals

What it is: Carrier-specific questionnaires that supplement the ACORD application with additional underwriting questions. Each carrier maintains its own supplementals — usually called just "supps" in conversation — often per class of business. The WC supp for restaurants asks about cooking equipment and after-hours operations. The cyber supp asks about MFA, backups, and incident response. The contractor GL supp asks about subcontractor controls and hot work procedures. Often 5–50 questions per supp.

Why founders care: Supplementals are where carrier-specific underwriting actually happens. ACORD captures the universal basics; the supp captures what makes this carrier different from the carrier next to it. Translating between ACORD data and a dozen different carrier supps — same question, different format, different field name, different position — is a substantial normalization problem and one of the highest-leverage places to add value in submission workflows.

How it shows up: A broker submits the ACORD 125 and gets back: "Need the supp." Twenty-five additional questions, half of them duplicating fields already on the ACORD but in a different format.

Key KPIs

GWP (Gross Written Premium)

What it is: Total premium written in a period, before any deductions for reinsurance ceded, commissions paid, or anything else. The headline top-line number for insurance companies, MGAs, and program administrators.

Why founders care: GWP is the standard way insurtech founders describe scale to investors. "$50M in GWP" tells you the volume of premium flowing through the platform, which — combined with commission rate — implies revenue.

How it shows up: "We did $30M in GWP last year" means $30M of policies were written. If commission was 12%, revenue was roughly $3.6M.

Bind Rate

What it is: The percentage of quotes that result in bound policies. Bind rate = bound policies ÷ quotes issued. Tracked weekly, monthly, by carrier, by product, by producer. A 20% bind rate means 1 in 5 quotes becomes a policy.

Why founders care: Bind rate is one of the cleanest funnel metrics in commercial distribution. It encodes quote quality, pricing competitiveness, and submission targeting all in one number. A sub-10% bind rate signals quotes that aren't competitive, submissions being routed to the wrong carriers, or risks being shopped too widely. A 40%+ bind rate suggests strong appetite-pricing match, but can also signal submissions being filtered too narrowly and revenue being left unwritten. Target ranges vary materially by line: small commercial (BOP, WC) tends to run in higher ranges, often 30%+; specialty and E&S typically run materially lower, often in the teens.

How it shows up: A retail broker reviewing a wholesaler relationship looks at bind rate alongside quote turnaround time. A 35% bind rate with a 4-hour quote turnaround wins more business. A 12% bind rate at a 5-day turnaround does not.

Commission

What it is: The percentage of premium paid by the carrier to the broker (and/or MGA) for placing the business. Rates vary by line and channel. Rough ranges: WC 5–10%, BOP/GL 10–15%, specialty/E&S 15–20%+. Negotiated, often confidential.

Why founders care: Commission is the revenue line for almost every insurtech that touches distribution. Understanding how it splits between MGA, wholesaler, and retail broker is essential to modeling partnership economics.

How it shows up: A retail agency selling a $10K BOP policy at 12% commission earns $1,200. If they bought the business through a wholesaler, $300 of that might go up the chain.

Loss Ratio

What it is: Incurred losses ÷ earned premium. The core measure of underwriting profitability. A loss ratio of 60% means the carrier paid $0.60 in claims for every $1.00 of earned premium. Most carriers target loss ratios in the mid-fifties to mid-sixties, though targets vary meaningfully by line.

Why founders care: Loss ratio is the metric carriers watch when evaluating an MGA program. A program running at 45% loss ratio gets renewed, increased capacity, and override commission. A program running at 75% gets non-renewed.

How it shows up: "The program ran at a 52% loss ratio over three years" is the sentence that makes a carrier commit more capacity.

Override

What it is: Additional commission paid to an MGA or wholesaler on top of base commission, typically structured as a percentage of premium or a profit-share tied to loss ratio. Sometimes called "contingent commission" or "profit commission." The terms differ technically but get used interchangeably.

Why founders care: Overrides are where MGA economics get interesting. Base commission keeps the lights on; overrides drive valuation.

How it shows up: "We get a 5% override plus 25% profit share above a 60% loss ratio." The structure of an MGA's upside.

Key Technology Providers

PAS (Policy Administration System)

What it is: The carrier's system of record for policies: quoting, issuance, endorsements, billing, renewals, claims-feed integration. Examples: Duck Creek, Guidewire PolicyCenter, Majesco. PAS replacements are typically 5–7 year projects costing tens of millions.

Why founders care: PAS is the bottleneck behind every carrier API. The carrier's API is essentially a window into their PAS, with all of the PAS's limitations baked in. If the carrier's PAS doesn't support a feature, no API will give it to you either.

How it shows up: A carrier says "we can't do mid-term endorsements via API because of how our PAS handles them." That's a PAS limitation, not an API limitation.

AMS (Agency Management System)

What it is: The retail agency's system of record. Manages clients, policies, renewals, commissions, customer service workflows. Vertafore AMS360, Applied Epic, EZLynx, HawkSoft are the major players.

Why founders care: If your product is sold to retail agencies, the AMS is where it has to integrate. AMS data ownership and integration depth are existential issues for any retail-facing insurtech.

How it shows up: A retail agency evaluating your product asks: "Does it download to my AMS?" If the answer is no, you're going to lose to a competitor whose answer is yes.

IVANS

What it is: The industry-standard data download network operated by Applied Systems. Carriers push policy data — declarations, endorsements, billing, commissions — to retail AMS systems via nightly IVANS downloads. Functionally, IVANS is the carrier-to-agency data backbone for the entire US retail market.

Why founders care: IVANS is invisible infrastructure that the retail channel depends on. Any product purporting to move data between carriers and agencies will either work with IVANS or get measured against it.

How it shows up: A retail agency's morning ritual: open the AMS, check what downloaded overnight from IVANS: new policies bound, endorsements processed, commission statements issued.

Carrier Connectivity Infrastructure

What it is: The infrastructure layer that gives a platform unified API access to multiple carriers behind a single connection. Underneath, the provider handles per-carrier data model translation, underwriting question mapping, authentication, monitoring, and ongoing maintenance, so the platform built on top connects once and accesses the full network. A category that has emerged over the past several years; CoverForce is one example.

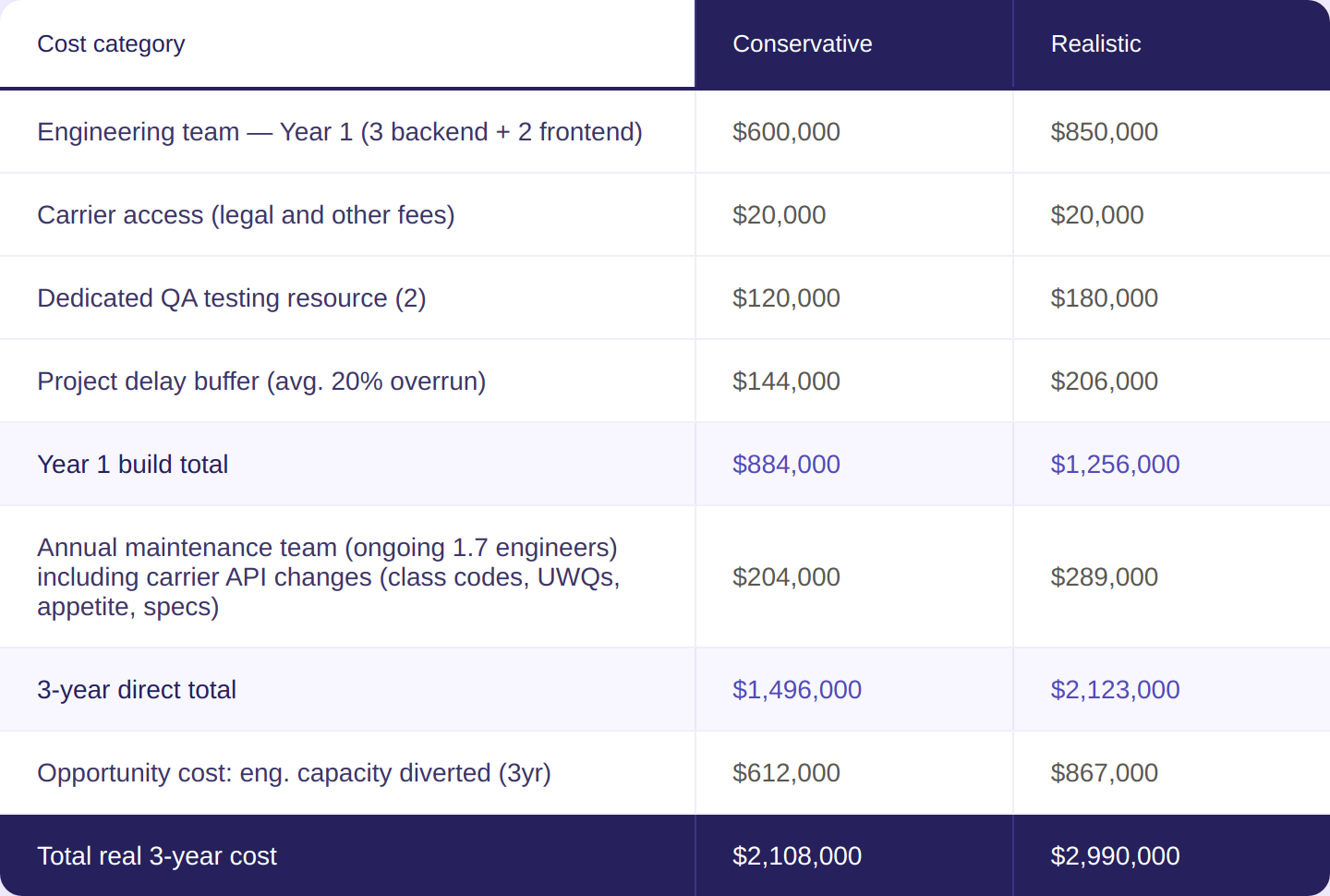

Why founders care: Building carrier connectivity in-house is expensive and ongoing. Each integration takes months, sometimes longer for complex carriers; once shipped, it continues to consume engineering capacity because carriers change their APIs, deprecate endpoints, launch new products, and retire old ones. Platforms that start by building their own connections often reassess the buy-vs-build math 12–18 months in, after the maintenance load has outgrown the original roadmap.

How it shows up: A platform planning to quote across multiple carriers in multiple LOBs faces an early choice: build the integrations in-house, sub-appoint through a wholesaler whose tech and appointments are already in place, or connect through a CCI provider. The choice shapes the engineering org for years afterward.

A Final Note

This list will keep evolving. If there's a term you keep tripping over that isn't here, send it over and we'll add it.

For founders building in commercial insurance, the language is the moat. The faster you can speak it fluently, the faster you can have the conversations that move deals.

And if you're building distribution and want to skip the part where you spend two years building carrier API connections yourself — reach out. It's what we do.

.png)

.jpg)

.jpg)